In the last few years, cryptocurrencies have come out of the shadows and are looking to take a stroll down main street. It’s been a volatile journey that still leaves many bankers wondering, “What is crypto all about and what can it do for us?”

What Damage Could Cryptocurrencies do to the Financial Sector?

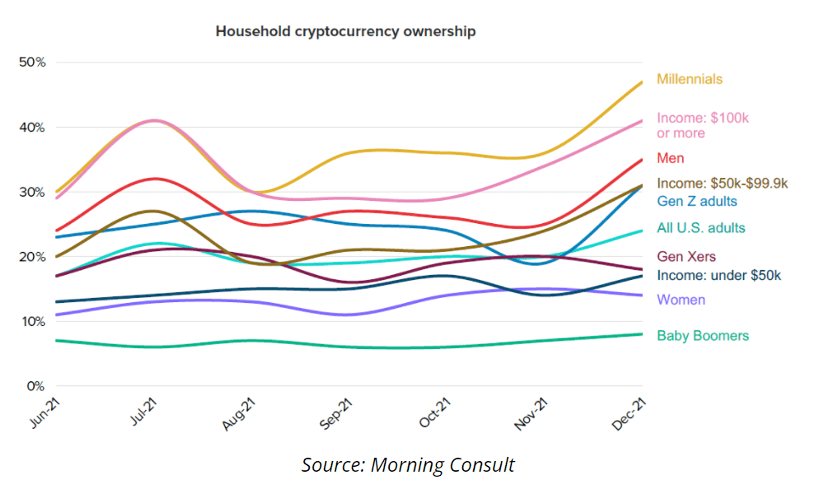

The growing popularity of cryptocurrency could cause a decrease to financial institutions’ core deposits. This is a present-day concern that only has larger implications in the future. Currently, millennials are the second largest generation and are the children of the largest generation – the baby boomers. As wealth begins to transfer from the baby boomers to the millennials, their economic power is going to increase.

The millennials along with Gen Z, the generation coming behind them, embrace cryptocurrency. If financial institutions do not find a path to incorporating cryptocurrencies or an equally innovative product into their product mix, they risk losing a generation of customers and put their own future at risk. Core deposits represent a low-cost funding source and decreased levels will impact the financial institution’s ability to fund other strategic initiations.

In the future, the cryptocurrency use cases will continue to develop. Decentralized finance (DeFi) is a financial tool that allows proof of ownership without the third party that was previously the source of trust. This is accomplished by making a digital token of anything, be that money, physical property, or a promise (smart contracts). Tokenization and smart contracts’ potential power allows for endless use cases including peer-to-peer lending, digital identity verification, alternative credit reports, and off-exchange investment trading. Some of these use cases present great benefit to traditional financial institutions, but DeFi also provides the potential to eliminate financial institutions’ traditional role. If DeFi potential is realized it will intensify competition and disruption.

The current-day issue may be tempting to ignore. There is a generation of customers that still embrace traditional banking, but the threat is only going to grow. The pandemic highlighted how even those who would typically use traditional in-branch services can and will adapt to new technology. Now that everyone has had some exposure, there will be increased pressure to adopt innovative products and services.

Why Should Financial Institutions Embrace Cryptocurrency?

Currently, crypto companies are unable to offer traditional cash management products and are eager to partner with a financial institution. Some of these crypto companies will get their own banking charters but most will look to partner with an established financial institution. A partnership will allow the financial institution to retain their core deposits and offer customers an innovative product. Such a partnership will allow the financial institution to continue doing what it does best and provide expertise to the partner about regulation and banking operations.

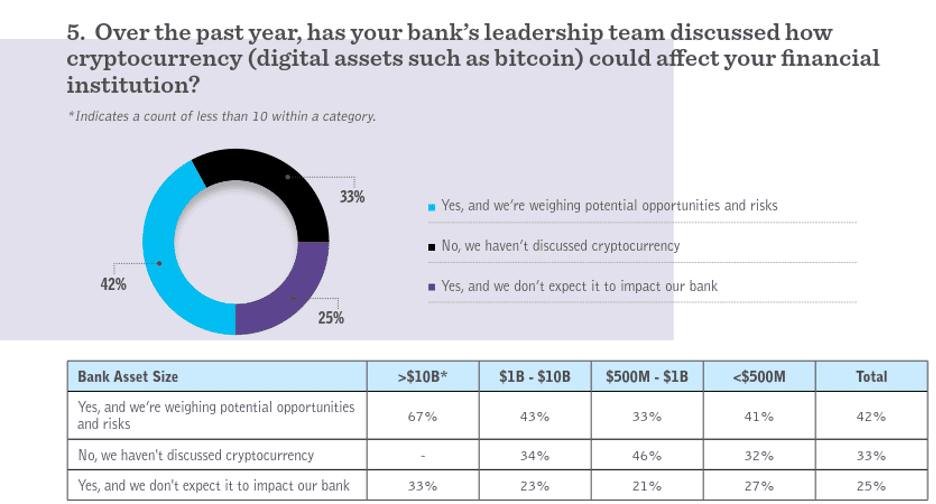

There are limited financial institutions in the space, which means there is an opportunity to capitalize on this growing trend. As shown by the survey results from Bank Director below, there is still time to be a first mover in this space.

Source: Bank Director 2021

In addition, given the volatility and popularity of cryptocurrency, more regulation in this space is a certainty. The only question is how soon it will come and what form it will take. A significant, sustained crash or other negative event in the crypto space will expedite the timeline. Upcoming regulation will begin to level the playing field and make partnering with a crypto company less risky for financial institutions. It will also increase the need for crypto companies to partner with someone with a strong compliance program.

Taking the First Step

To truly embrace the coming crypto transformation, financial institutions need to designate a leader who can review and monitor the evolving landscape and spearhead new initiatives. Institutions may call this a Chief Innovation Officer, Emerging Risk Officer, or other title. Whatever you call the role, it is critical that they are responsible for the following:

Monitor fintech activity and find strong companies to partner with

Work closely with the financial institution’s compliance management system to stay abreast of crypto regulation and SEC action

Monitor developments related to Central Bank Digital Currencies (both US and other developed countries)

Perform new product / partnership risk assessments

Establish governance including risk appetite, cryptocurrency policy creation, and ongoing oversight

Bottom Line

This is a dynamic time in banking. The road ahead may not be clearly laid out but the opportunities in cryptocurrency are going to be significant. Financial institutions need to begin setting the foundation and create a path toward a collaborative relationship now, or it will be too late.

Additional reading regarding the risks and opportunities: